THE WORLD GAME OF ECONOMICS: LESSON 4

Focus on Macroeconomic Policy

NOTE: It is highly recommended that you read over this entire lesson before you begin.

Preliminary Discussion: The combined forces of Aggregate Demand and Aggregate Supply determine the level of output, prices, and employment for countries in the global economy. Aggregate Demand (AD) is the amount of total spending on the part of consumers, businesses, government, and net exports at different prices. Spending is inversely related to prices. Aggregate Supply is the amount of output on the part of producers at different prices. Production is directly related to prices. The equilibrium level of output and prices for a given economy is where Aggregate Demand is equal to Aggregate Supply.

Aggregate Demand schedules will move to a different location whenever there is a change in one or more of the following variables: consumer and business expectations, consumer wealth and/or indebtedness, taxes, interest rates, government spending, exchange rates, and economic activity in trading partner nations.

Aggregate Supply schedules will move to a different location whenever there is a change in one or more of the following variables: cost of resources, technology and productivity, business taxes, and government regulations.

Aggregate Demand and Aggregate Supply schedules are constantly in motion. Whenever either Aggregate Demand or Aggregate Supply change, the economy moves to the new equilibrium at the intersection of the two schedules. This is what causes business cycles and fluctuations in output, prices, and employment for a given economy.

Economic policy affects Aggregate Demand and Aggregate Supply. The role of economic policy is to observe the direction of economic activity and undertake steps to improve the country's overall economic performance. Generally, the goals are to achieve full employment, price stability, and economic growth without excessive pollution. Fiscal, trade, and monetary policy tools are used to achieve an acceptable balance of conflicting goals.

In The World Game of Economics you are the chief economic adviser to the leaders of the country of your choice. You are in charge of economic policy. The objective is to implement timely and appropriate economic polices to improve the overall economic performance of your country. Good luck and have fun!

1. Play The World Game of Economics to 100 points against up to six other countries that are computer-managed (i.e., advised by Professor N. D. Cator) or Laissez Faire. Note: If you do not know how to play the game, then select "Tutorial" from the main menu first. If you already know how to play, then select "New Game."

2. You are the chief economic adviser to which country?

_______________________.

3. How many other computer-managed countries are you playing

against? ________.

SOMETIME AFTER THE 3RD YEAR AND BEFORE THE 10TH YEAR OF THE GAME COMPLETE THIS EXERCISE:

4. Which year have you chosen to complete this exercise?

__________.

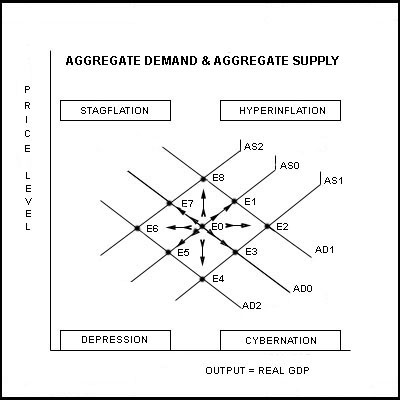

5. Look at the Aggregate Demand and Aggregate Supply diagram

below. Assuming your economy is at E0 at the beginning of your turn,

which direction is the Economic Indicator currently pointing: (Circle

One)

E1 E2 E3 E4 E5 E6 E7 E8

6. Which change or combination of changes in Aggregate Demand and Aggregate Supply does the direction of the Economic Indicator predict? (Circle One)

+AD +AD&+AS +AS -AD&+AS -AD -AD&-AS -AS +AD&-AS

7. Click on the ECONOMIC INDICATOR and the CURRENT EVENT. Next, click on ECONOMIC POLICY to go to the Policy Board. What score would you get at this time if you could not select economic policies? My score would be: _____.

9. Now SELECT YOUR ECONOMIC POLICES. What score did you get for this turn? My score for this turn was: _____. Compared to my answer to Number 7 (above), my score [___ improved] [___ got worse] [___ did not change] because of my policies.

10. COMPLETE THE GAME. Print the final score and attach it to this exercise.

ANSWER QUESTIONS 11 15. (Circle the letter before the best single answer).

11. According to Keynesian theory, whenever an economy is in a recession

or Depression caused by a decline in consumer spending and business investment,

the most effective economic policy to counteract this trend is:

(a) industry deregulation.

(b) raise taxes.

(c) do nothing.

(d) increase government spending.

(e) implement price ceilings.

12. Stagflation poses a demand-side policy dilemma for the government,

because:

(a) If the government implements price ceilings, then prices and production

both fall.

(b) If the government increases spending and the money supply, it causes

more inflation; and if the government cuts spending and the money supply,

it causes more unemployment.

(c) If the government deregulates industry and banks, then prices and

unemployment both increase.

(d) If the government does nothing, then prices will rise further;

and if the government does something, then cyclical unemployment will increase.

(e) If the government increases spending and decreases the money supply,

then inflation will increase, production will fall, and more workers will

be frictionally unemployed.

13. The most effective policies to curtail Hyperinflation are:

(a) price floors.

(b) industry deregulation

(c) industry regulation.

(d) tax cuts and tariffs.

(e) cut the money supply and government spending.

14. The social benefits of more Entitlement programs probably exceed

the social costs, when:

(a) the economy has low prices (or deflation), and there is high unemployment.

(b) the economy has high prices (or inflation), and there is low unemployment.

(c) the economy is producing as much as it can, and there is too much

pollution.

(d) the economy is in Stagflation, because the minimum wage is too

low.

(e) the economy is in Hyperinflation, because there is too much money

in circulation.

15. It is difficult to implement economic polices to fine tune the economy

and land in the center of the playing area of The World Game of Economics,

because:

(a) You're never really certain where the economy is or where it's

headed.

(b) Economists don't really understand how the economy works, and they

never will.

(c) You don't always have the right fiscal policy options, it's difficult

to coordinate the timing of policies, another country's trade policy affects

your economy, and the multiplier effect is unpredictable.

(d) You can't be sure that if you increase government spending, the

economy will actually expand; and if you increase the money supply, prices

may go up or down as a result.

(e) The Economic Indicator is extremely unreliable, and Professor N.D.

Cator cheats.

End of Lesson 4

Note: At the instructor's discretion, you will receive _____ possible points for this exercise.

Instructor's Option: At the instructor's discretion, you may receive additional points according to the schedule below.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|||

|

|

|

|

||||

|

|

|

Examples: If you play against 6 other countries and you place 1st, then you get 10 extra points! If you play against 4 other countries and you place 3rd, then you get 6 extra points. If you play against two other countries and you place 2nd, then you get 5 extra points. In each case if you place last, then you get only 4 more points.

Winning Strategy Hints: Winning strategy involves anticipating

the Economic Indicator, playing your policy options efficiently, coordinating

your range of policies, and using trade policy to prevent one country from

getting too far ahead. Consider your opponents options and try to

anticipate their trade policies. Keep in mind that countries tend

to use trade restrictions, tariffs, and currency devaluations when they

have high unemployment. Be careful not to get caught having too many inappropriate

and useless options. Discard policy gridlock and foreign policy conflict

options as frequently as possible. [You dont want to be trapped

in a Depression like the United States in the 1930s or caught like Germany

in Hyperinflation in the early 1920s]. Study the probabilities that

are provided in the instructions. That will help you plan your strategy.

The World Game of Economics (C) 1999 Ronald W. Schuelke

All Rights Reserved