Source: Kitco Precious Metals http://www.kitco.com

NOTE:

April 2012 -- There is a brief explanation of gold's surge in price in

recent years at the end of this article.

NOTE:

April 2012 -- There is a brief explanation of gold's surge in price in

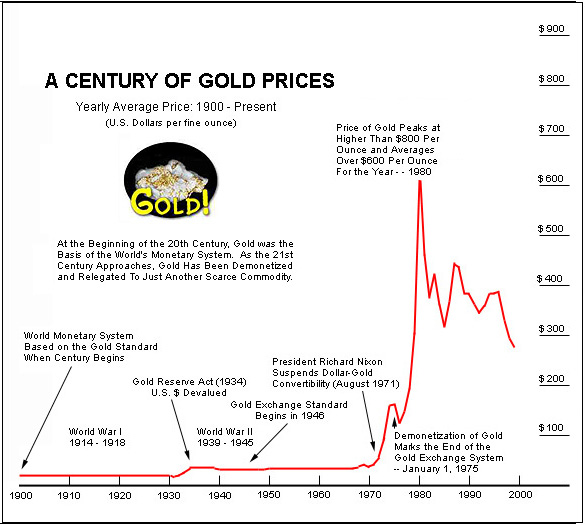

recent years at the end of this article.Ever since gold was demonetized in the 1970s, gold prices have been riding a roller coaster -- up, down, way up in 1980, then down, back up again, and then mostly down. When the gold exchange system was officially abandoned in 1975, gold prices became determined by free market forces. Normally, gold prices fluctuate as a result of speculation on the demand side. However, the recent decline in prices is primarily attributed to increases in supply. Technological change has increased productivity in gold mining, and central banks around the world are selling off their gold stocks. When the supply of gold increases, prices fall.

Early in July the Bank of England auctioned 25 tons of British gold, and it announced plans to sell more in the future. Canada, Belgium, and the Netherlands have all sold gold recently, and Switzerland intends to dump another 1,300 tons onto the gold market. At the Economic Summit in Koln, Germany the G-7 countries tentatively agreed to sell more of the International Monetary Fund's gold, invest the proceeds, and use the interest income from the new investments to help the world's heavily indebted poor countries.

The policy of central banks dumping gold at the end of this century is a sharp contrast from their attitude toward gold at the beginning of this century. [See Chart Below]. Early in the 1900s the world's monetary system was based on the gold standard. Gold was considered to be a prize possession by individuals and national treasuries. Under the gold standard, a nation's money supply consisted of gold and currency backed by gold. The price of gold was officially set by governments at $20.65 per ounce, currency could be exchanged for gold, and gold moved freely across international boundaries.

The gold standard was designed to keep consumer prices stable. An economy would not experience inflation unless the gold supply increased, and that was unlikely since gold was relatively scarce. The system also presumed a self-correcting process regarding the effects of international trade. If a nation exported more than it imported, gold would flow into the country, prices would rise, imports would go up, and exports would fall. If a country began to import more than it exported, gold would flow out of the country, prices would fall, imports would go down, and exports would rise.

The efficacy of the gold standard was undermined by the growth of demand deposits as the principle form of money, periodic suspensions of currency convertibility into gold (especially during war time), and the fact that adjustments often affected output more than the price level. Wages and prices were resistant to falling, so a decline in the money supply had a more visible effect on falling output and rising unemployment. Deflation became almost synonymous with depression.

Source: Kitco Precious Metals http://www.kitco.com

Still clinging to the basic principles of the gold standard, the United States passed the Gold Reserve Act in 1934. This gave the U.S. government title to all monetary gold in the country. Ordinary citizens were prohibited from owning monetary gold, and the dollar was devalued from $20.67 to $35 per ounce. The devaluation was supposed to increase U.S. exports and help the economy out of the Great Depression, but its effects were negligible and it didn't work.

After World War II, the leading industrialized countries established the gold exchange standard in 1946. Under this system, the United States' gold stocks were used to back the world's currencies. The other countries' currencies were pegged to the U.S. dollar, and central banks could convert dollars into gold at $35 per ounce. Over time, however, chronic U.S. balance of payments deficits caused the supply of dollars abroad to exceed the U.S. stock of monetary gold at the official rate of $35 per ounce. It became increasingly clear that the U.S. dollar was an over valued currency, and some nations began to convert their dollars into gold. The U.S. Treasury's stock of gold diminished significantly.

The rapid decline in U.S. gold reserves reached a crisis in 1971, and President Richard Nixon suspended the dollar-gold convertibility. This event marked the end of gold as an international monetary instrument. It effectively demonetized gold, and four years later on January 1, 1975 the world officially abandoned the gold exchange standard. The International Monetary Fund terminated the use of gold, the word "gold" was expunged from international agreement, and the 41 year ban on gold ownership in the United States was ended. Gold became just another scarce commodity with virtually no official link to the international monetary system. Currency exchange rates began to fluctuate freely. For a while, the value of the dollar fell and the value of gold rose to unprecedented heights, peaking at just over $800 per ounce in 1980.

Sixteen years earlier, the movie version of Ian Fleming's novel Goldfinger had been released. The plot was fascinating and intriguing with gold at its center. Goldfinger was an industrialist who was discreetly buying up gold. His plan was to detonate a nuclear device at Fort Knox, Kentucky where the United States gold reserves were held. If everything went as planned, the gold in Fort Knox would be rendered useless. This would significantly decrease the available supply of gold, the world's monetary system would be thrown into chaos, and gold prices would skyrocket. Goldfinger estimated that the gold he had been purchasing would increase in price ten-fold. Of course, British agent James Bond (007) foiled the plan and the world's monetary system was not disrupted. But perhaps the movie was an omen, because the price of gold did rise dramatically in the 1970s although for entirely different reasons.

Now we are witnessing the opposite of the goldfinger effect. The available gold supplies are not decreasing. They are increasing and rather dramatically. As one central bank after another releases its gold stocks to the private market, gold prices are plunging. Of course, everybody is asking: When will gold prices hit bottom?

There is a basic principle in economics that suggests the price of a commodity like gold exchanged in a competitive market will move to an equilibrium price that is just sufficient to reward the most efficient producers a "fair return" on their investment. Demand is a key variable. If the demand side of the market is willing to pay a given price for gold, then gold markets will meet that demand if possible. According to today's gold producing experts, if the price of gold stays below $260 per ounce, many gold mines will either close down or cut back production and lay off workers. Gold that is harder to find and requires more dirt to be moved for every ounce of gold reclaimed is not profitable when gold prices fall. Meanwhile, if gold mines are in competition with the demonetization of gold and central banks that are dumping their gold stocks, then gold prices will fall even further in the near future.

However, as long as gold retains its mystique and if speculators

begin

to believe that its price will rise again, then it's possible for gold

prices to eventually recover.

UPDATE:

Since the

original publication of this article in July 1999, the price of gold

rose persistently and at times

exponentially for the next 12 years. In

April 2012 the price of gold hovered around $1650 per ounce! The most common explanations for gold’s

dramatic surge in value are the following:

1. Expectations of global inflation in the long run have

induced savers and speculators to purchase gold as a hedge against the

possibility future inflation. Gold has

historically been a safe haven during inflationary spirals, because its

value

goes up and money’s purchasing power falls.

The basis for the expectations of future inflation is a

combination of

chronic deficit spending by industrial nations’ governments and their

central

banks’ proclivity to accommodate the deficits (aka “monetization”) with

higher

than average increases in the money supply.

Under some circumstances the combination of fiscal deficits and

expansion of the money supply can initiate and fuel demand-pull

inflation.

.Maybe it would be time to cash in your gold

and invest in a yacht. There are beautiful yachts for sale.

A yacht may even be a viable option for

retirement for some.

The World Game of Economics, The Global Economics Game (C) 1999, 2004, 2012 Ronald W. Schuelke All Rights Reserved