The Foreign Exchange Market

The Foreign Exchange Market

The international foreign exchange market operates around the clock It opens on a Monday morning in Hong Kong, while it is still Sunday night in San Francisco. Throughout the day, markets begin trading in Tokyo, Zurich, Frankfurt, Paris, London, New York, Chicago, and finally the West Coast of the United States. When the markets close in Los Angeles and San Francisco on Monday evening, Hong Kong is one hour away from beginning foreign exchange trading on Tuesday.

CLICK ON THE IMAGE BELOW

TO GET THE LATEST

FOREIGN

EXCHANGE

QUOTATIONS

Currency Converter

[Note: This Currency Converter is provided with the

permission

and through the courtesy of Xenon Laboratories]

In The Global Economics Game you have the power and influence of a central bank to deliberately intervene in the foreign exchange market to either appreciate or depreciate your nation's currency.

The Foreign Exchange Market

![]()

The foreign exchange market is the monetary nexus between countries

that makes it possible for international trade to be accomplished more

efficiently than barter. Because each nation uses its own

monetary

unit, people in one country who want to purchase something in another

country

must exchange their own currency for the other to accommodate the

transaction.

Many travelers

research foreign exchange rates before purchasing airline tickets or

other means of travel to other countries. The foreign

exchange market is where one nation's currency is traded for another.

Exchange

rates can also affect your credit cards while visiting different

countries. Somc credit cards

may have a different exchange rate. Some cards may also charge

foreign transaction

fees while outside your home country. The top credit cards

won't charge these fees and will have consistent exchange rates.

You will fine infor online about what top credit card is best for you

and your travels.

On

any given day approximately $1.5 trillion in foreign exchange is

traded!

By any standard, that's a lot. The figure dwarfs the value of

daily

global stock trading. It is almost 20% of the United States GDP

and

nearly the size of the U.S. federal budget for an entire fiscal year.

Contrary

to what many people think, most foreign exchange trading is not in

currencies,

per

se. Rather, it is in the form of bank deposit balances.

Also, a surprisingly small number of banks account for the bulk of the

volume, and nearly 90% of all trades involve U.S. dollars.

On

any given day approximately $1.5 trillion in foreign exchange is

traded!

By any standard, that's a lot. The figure dwarfs the value of

daily

global stock trading. It is almost 20% of the United States GDP

and

nearly the size of the U.S. federal budget for an entire fiscal year.

Contrary

to what many people think, most foreign exchange trading is not in

currencies,

per

se. Rather, it is in the form of bank deposit balances.

Also, a surprisingly small number of banks account for the bulk of the

volume, and nearly 90% of all trades involve U.S. dollars.

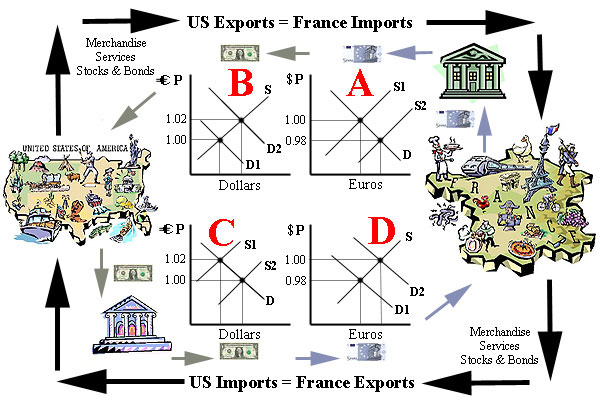

Although a few countries officially fix the exchange value of their currency to a key currency or basket of currencies, the exchange rate between most currencies is primarily determined by the market forces of supply and demand. When people in Europe supply euros to demand dollars in order to purchase U.S. products, the exchange value of the euro depreciates and the dollar appreciates, all other things held constant. If the supply of a currency exceeds the demand for it, its value will fall in the foreign exchange market. On the other hand, if the demand for a currency exceeds its supply, then its value will rise. An increase in the supply of one currency is simultaneously an increase in demand for the other. The picture below shows how this works in the context of international trade.

(A) French citizens supply euros to their banks and demand dollars to import goods and services from the United States. The value of the euro falls from $1.00 to $0.98. (B) Simultaneously, the value of the dollar appreciates from 1.00 to 1.02 euros. (C) U.S. citizens supply dollars to their banks to demand euros to import goods and services from France. The value of the dollar falls from 1.02 euros to 1.00 euro. (D) Simultaneously, the euro returns to equal $1.00. If supply and demand for the two currencies balance, then the exchange rate between the two currencies will remain stable. Exchange rates fluctuate when the relative supply and demand schedules do not balance.

To really understand how the market determines

whether the euro is worth $0.98, $1.00, or $1.02, one needs to look at

the participants and the underlying market forces driving their

decisions.

The principal players or participants in the foreign exchange market

are

companies and persons who engage in international commerce and their

banks,

foreign investors, currency speculators, and central banks.

Somewhat

surprisingly, less than 20% of all foreign exchange transactions are

directly

linked to the needs of importers and exporters of internationally

traded

merchandise and services.

Over 80% of the transactions involve

short-term

speculation and the purchase of foreign financial investments.

Occasionally,

central banks intervene in the foreign exchange market to deliberately

manipulate the exchange value of their nation's currency.

[You may wish to visit Alpari to view fundamental information about Forex and trading within the FX market and learn the definitions and intricacies of base and quote currencies].

The relative supply and demand schedules for any two currencies on the part of these participants are a function of population, consumer tastes, disposable incomes, the relative price levels in the two countries, peoples' expectations regarding future prices and exchange rates, the relative rates of real return on financial investments, and the objectives of central banks. We can formulate the following generalizations for each of these variables (assuming the others are held constant):

1. A country with a large population will

demand

more currency from a country with a small population than vice versa.

2. People will demand more currency from another

nation when they find its products to be more appealing.

3. Countries with high and rising incomes will

demand more foreign currency than countries with low incomes or those

that

are in recession.

4. Relatively high domestic inflation in a

country

will curtail the demand for its currency.

5. If importers expect prices in the exporting

country to rise in the future, they will demand more of that currency

in

the present to beat the price increases.

6. People will demand more of a foreign currency

if they can get a higher rate of return on financial investments in

that

country.

7. On the other hand, if foreign investors expect

that inflation will undermine the real return on their investments in a

country, then they will get rid of that currency and move their money

to

another country.

8. If people expect a currency to appreciate

in the future, they will demand more of that currency in the present.

9. Central banks will demand more of a foreign

currency if they wish to depreciate their own.

While these generalizations can be applied to analyze short run fluctuations in exchange rates, there are two prominent theories that economists use to explain and predict exchange rate trends over the long run. One is the purchasing power parity theory and the other is referred to as the monetary approach.

The purchasing power power parity theory suggests that exchange rates tend to adjust so that a person will have the same purchasing power to buy goods and services in another country after the exchange that he/she had with his/her own money in the home market before the exchange. The theory is founded on the law of one price which states that a commodity like a loaf of bread will, in effect, be the same price any where in the world if markets operate efficiently. Thus, if bread costs $1.00 per loaf in the United States and 100 yen in Japan, then the exchange rate will move toward $1.00 = 100 yen (and 1 yen will equal $0.01). Applying this theory, one would predict that relatively high inflation in one country will cause its currency to depreciate in the long run. This theory seems to predict reasonably well if one confines the analysis to internationally traded commodities. It tends to be nearly useless if the market basket of goods and services used to measure the price level includes many that are not traded internationally. Housing, auto insurance, gasoline, haircuts, evening dining, video rentals, entertainment, and other local services are examples.

The monetary approach to exchange rate determination in the long run looks at the relative change in the money supply of two (or more) nations. In a sense, this is even more fundamental than the purchasing power parity theory, because money supplies affect prices. The monetary approach is built on the quantity theory of money which states that prices will rise in a country that increases its money supply faster than the rate of change in real GDP. Thus, if a country's real GDP can only increase at a rate of 4 per cent and the money supply is increased by 6 per cent, then the price level will rise by 2 per cent and the country's currency will depreciate accordingly in the foreign exchange market (assuming other countries are only increasing their money supplies by 4 per cent and their price levels are remaining stable). Looked at another way, if a country is increasing its money supply at 4 per cent and real growth is 6 per cent, then the price level will fall and the country's currency will appreciate in foreign exchange markets (assuming other countries are increasing their money supplies and their economies are growing at 4 per cent). The main conclusion(s) of the monetary approach is that countries which maintain relatively restrictive monetary polices and/or experience relatively rapid increases in productivity will see their currency appreciate in foreign exchange markets over the long run.

Not all countries allow the exchange rate of their currency to fluctuate. Some countries officially fix or peg their currency to another key currency or a basket of currencies. In fact, the International Monetary Fund (IMF) identifies 10 classifications of exchange rate arrangements around the world -- ranging from those that are pegged, to those that crawl, to those that are market driven. Argentina, China, Egypt, Hong Kong, Saudi Arabia, and Vietnam are examples of countries that peg the exchange rate of their currencies to the U.S. dollar. Israel, Poland, Turkey, and many countries in Latin America fall into the crawling peg category. This means that the official exchange rate is automatically adjusted according to a predetermined formula. Australia, Brazil, Canada, India, Japan, Korea, Mexico, New Zealand, South Africa, Sweden, Switzerland, the United Kingdom, the Euro area countries (Germany, France, Italy, Spain, Netherlands, Belgium, Austria, Finland, Greece, Portugal, Ireland, and Luxembourg), and the United States are the major countries whose currency exchange rates are largely market driven.

The main advantage of a fixed exchange rate system is that it (ostensibly) removes the risk of adverse exchange rate movements when planning to purchase foreign goods, services, and investments. When it works reliably, it encourages more participants in international trade. However, it has a mixed track record. The Bretton Woods System put into place after World War II was a fixed exchange rate system, and it worked reasonably well for about 2 decades. However, it collapsed in 1971. Currencies around the world had been pegged to the U.S. dollar and the dollar was convertible into gold at $35 per ounce. When it became clear that the dollar had evolved to an over-valued currency at the fixed rates, central banks began to dump their dollars in exchange for U.S. gold. When President Nixon closed the gold window, an international currency crisis ensued, and the dollar plummeted in a floating exchange rate market.

The

problem with pegged exchange rate systems is that the rates don't stay

fixed. The foreign exchange market itself is more powerful and

seems

to find ways to unhinge them. The system requires a country to

maintain

large reserves of foreign currencies to supply the market when there is

an excess demand for them at the official exchange rate. Capital

flight occurs when investors fear that inflation or an inevitable

currency

devaluation will undermine the real rate of return on their

investments.

When the reserves are depleted, there is a currency crisis, and

the country is forced to let its currency devalue and find the market

equilibrium.

The most recent examples of this occurred in Asia in 1997, Russia in

1998,

and Brazil in 1999.

The

problem with pegged exchange rate systems is that the rates don't stay

fixed. The foreign exchange market itself is more powerful and

seems

to find ways to unhinge them. The system requires a country to

maintain

large reserves of foreign currencies to supply the market when there is

an excess demand for them at the official exchange rate. Capital

flight occurs when investors fear that inflation or an inevitable

currency

devaluation will undermine the real rate of return on their

investments.

When the reserves are depleted, there is a currency crisis, and

the country is forced to let its currency devalue and find the market

equilibrium.

The most recent examples of this occurred in Asia in 1997, Russia in

1998,

and Brazil in 1999.

On the other hand, the problem with a flexible exchange rate system is the high risk associated with market fluctuations. Suppose, for example, someone in the U.S. were to take their dollars, buy British pounds, and deposit the pounds in a British bank to earn an 8 per cent return. If the value of the British pound were to depreciate by 12 per cent, then the investor would lose 4 per cent when converting the pounds back into dollars. This possibility discourages many people from making foreign investments. And there is economic turmoil when those who were not dissuaded from international investment lose as a consequence of adverse currency movements.

The shortcomings of the fixed exchange rate system and the free floating system have led the world's governments to attempts at international policy coordination and a system referred to as a managed float (sometimes called a dirty float). Under current arrangements, most countries let their currency exchange rates fluctuate according to market forces as described above. However, if a currency appears to be "overvalued" or "undervalued" by the market, or if the exchange rate movements are significantly adversely affecting an economy's macroeconomic performance, or if the policy-makers wish to use exchange rate manipulation to achieve a macroeconomic objective, then central banks will intervene in the foreign exchange market to deliberately depreciate (or appreciate) their currency. For example, the Plaza Agreement in 1985 involved central bank intervention to deliberately depreciate the U.S. dollar, because its high exchange value was retarding U.S. exports. Later, in 1987 the Louvre Accord sought to stabilize the dollar to prevent it from falling further.

Although no major coordinated intervention has occurred recently, individual central banks have intervened to affect the exchange value of their currency. The most recent example occurred in late 1999, when the Bank of Japan dumped yen into the foreign exchange market to prevent its value from rising further. When the Bank of Japan supplied yen to the foreign exchange market, it demanded dollars and the value of the dollar rose as the value of the yen fell. The central bank did this, because the high and rising value of the yen had begun to retard Japanese exports and the economy was already in recession. Depreciating the yen would stimulate Japan's exports and the Japanese economy.

In The Global Economics Game you have the power and influence of a central bank to deliberately intervene in the foreign exchange market to either appreciate or depreciate your nation's currency. If you depreciate your currency, your exports will increase and your imports will decrease. Your economy will grow faster, but prices will rise. If you appreciate your currency, your exports will fall and your imports will rise. The price level will fall, but the economy will contract.

Recommended:

IMF

Staff. Exchange Rate Regimes in an Increasingly Integrated World

Economy

(June 2000).

Return to Home Page Overview/Feedback/Awards How To Play/Features Information for Educators

Scholarship Contest World Economics News

The World Game of

Economics

(C) 1999 Ronald W. Schuelke All Rights Reserved

The Global Economics

Game

(C) 2000-2004-2012 Ronald W. Schuelke All

Rights Reserved